Notary Blog

A Comparative Research Analysis of Major U.S. Bank Notarization Policies

ONE SIZE DOES NOT FIT ALL:

A Comparative Research Analysis of Major U.S. Bank Notarization Policies

Executive Summary

A widespread consumer assumption exists that banks are a universal, reliable, and freely accessible solution for notarization needs. This research challenges that assumption head on. After examining the publicly stated and operationally observed policies of ten major U.S. banks, this paper demonstrates a clear and consistent pattern: there is no standardized approach to notarization across American banking institutions.

The evidence reveals that each institution makes its own policy decisions regarding who can be served, which documents are eligible, when the service is available, whether appointments are required, and which notarial acts it will and will not perform. Consumers who rely on banks for notarization face unpredictable outcomes, limited access, and significant gaps in service, particularly for complex legal documents. These findings have direct implications for independent notaries, RON providers, and the general public seeking consistent, dependable notarization solutions.

Introduction

When most people think of notarization, the bank is the first place that comes to mind. It feels logical: banks are trusted, regulated institutions located in nearly every community. Yet the lived experience of millions of Americans tells a very different story. Customers are turned away because they are not account holders. Notaries are unavailable without advance appointments. Entire categories of legal documents are refused. Hours are limited to weekday banking windows, and entire branch locations may not staff a notary at all.

This paper examines the notarization policies of ten major U.S. banking institutions to make a clear argument: banks do not operate under any unified or standardized notarization framework. Each institution sets its own rules, and even within a single bank, policy enforcement varies by branch, by region, and by the individual notary on staff that day.

The practical consequence of this fragmentation is that millions of Americans face unnecessary friction when seeking notarization services, and that the banking system, despite its size and reach, cannot be relied upon as a consistent solution. This research is intended to inform consumers, legal professionals, and notary practitioners about the true landscape of bank notarization in the United States.

Methodology

Research for this paper was conducted using publicly available sources including official bank websites, published FAQs, legal service publications, and practitioner commentary. Policies were evaluated across the following six dimensions:

•Customer eligibility (account holder requirement)

•Fee structure for customers and non-customers

•Appointment requirements

•Operational hours and weekend availability

•Document types accepted and excluded

•Overall notary availability across branches

The ten institutions reviewed are: Bank of America, Chase, Wells Fargo, U.S. Bank, PNC Bank, TD Bank, Citibank, Capital One, Fifth Third Bank, and Huntington National Bank. Credit unions were reviewed separately as a distinct category.

Bank-by-Bank Policy Analysis

Bank of America

Bank of America has one of the more transparent and formal notarization programs among the major banks. The bank offers the service free of charge to its customers and requires that appointments be scheduled in advance. According to Bank of America's official notary services page, appointments are typically structured to run approximately 30 minutes and the notary reviews documents upon arrival to determine whether notarization can be completed.

Key policies include:

•Account holder requirement: Yes. Service is provided at financial centers to Bank of America customers.

•Fee: No charge for account holders.

•Appointment: Required. Scheduled through the bank's appointment system.

•Hours: Standard financial center hours, Monday through Friday. Limited Saturday availability at select locations. Closed Sunday.

•Documents: Customers are advised not to sign documents before arriving, and all signers must present state-acceptable ID. The notary determines at the appointment whether the bank is able to complete the notarization.

•Exclusions: The bank retains the right to decline if state or bank guidelines are not met. Estate planning documents, wills, and complex legal instruments are frequently declined due to liability policy.

Chase Bank

Chase Bank offers notary services at many of its branches as a benefit to customers. However, the bank does not maintain a formal appointment scheduling system for notarization across all locations, making access more variable than at Bank of America. The recommendation from Chase is to call ahead to confirm notary availability before visiting.

•Account holder requirement: Yes. Non-customers are generally not eligible, though individual branch policies can vary.

•Fee: Free for account holders.

•Appointment: No centralized system; walk-in with advance phone confirmation recommended.

•Hours: Standard banking hours, typically Monday through Friday 9 a.m. to 5 p.m. Some Saturday morning hours. Closed Sunday.

•Documents: Handles routine personal and financial documents. Will not notarize wills, trusts, international documents intended for use abroad, I-9 employment verification forms, or documents requiring apostille certification.

•Exclusions: Liability-driven refusals are common for estate documents. Some branches have contracted outside mobile notaries to supplement service, which introduces additional inconsistency.

Wells Fargo

Wells Fargo offers notary services to account holders at select branch locations. The bank recommends scheduling an appointment through its online system, though walk-ins may be accommodated depending on notary availability. Like other major banks, Wells Fargo's notary availability is not guaranteed at all branch locations.

•Account holder requirement: Yes. Non-customers do not qualify for free notary services.

•Fee: Free for customers.

•Appointment: Recommended; online scheduling available through the branch locator.

•Hours: Standard banking hours weekdays. Some locations open Saturday mornings. Closed Sunday.

•Documents: Standard financial and personal documents. Document must not be signed prior to appearing before the notary. All pages must be present.

•Exclusions: Estate planning documents, wills, and documents requiring witness coordination are frequently declined. Document complexity may result in refusal at the discretion of the on-site notary.

U.S. Bank

U.S. Bank provides notary services at select branch locations and treats the service as a customer benefit. Availability varies significantly by location and staffing. The bank's website directs customers to contact individual branches to confirm notary availability.

•Account holder requirement: Yes. Service is reserved for customers.

•Fee: Free for customers.

•Appointment: Recommended. Customers can schedule through the bank's branch appointment system.

•Hours: Standard weekday hours. Saturday availability is limited and location-dependent.

•Documents: General personal and financial documents.

•Exclusions: Not all branches staff a notary. Estate and complex legal document exclusions apply.

PNC Bank

PNC Bank provides notarization services to customers at most branch locations. The bank has an online appointment scheduling system that allows customers to book a time in advance. PNC is known for its broader availability across branch locations compared to some peers.

•Account holder requirement: Yes.

•Fee: Free for customers.

•Appointment: Available through the PNC appointment system online.

•Hours: Weekday banking hours standard. Some Saturday morning hours available.

•Documents: Standard documents covered. Bring all pages and do not sign before appearing before the notary.

•Exclusions: Estate planning documents and complex legal instruments are subject to refusal based on internal risk policy.

TD Bank

TD Bank is notable for having one of the more extended operating hours of the major banks, including evening hours at some locations and Sunday hours at select branches. This makes TD Bank somewhat more accessible than peers, though notary availability is still listed as a branch-specific service that varies by location.

•Account holder requirement: Yes. Service is limited to account holders.

•Fee: Free for customers.

•Appointment: Appointment booking is available and recommended.

•Hours: Branches vary. Some locations open as early as 8:30 a.m. and as late as 6 p.m. weekdays. Saturday hours common at 9 a.m. to 1 or 2 p.m. Select branches open Sunday.

•Documents: Standard service for personal and financial documents.

•Exclusions: Notary listed as a branch-level service; not all locations have it. Estate document exclusions apply.

Citibank

Citibank offers notary services at some branch locations, but availability is more limited compared to the other banks in this review. Customers must verify notary availability on the Services tab of their specific branch location before visiting, and an appointment is required.

•Account holder requirement: Yes.

•Fee: Generally free for customers, though some branches may charge depending on document type and state caps.

•Appointment: Required.

•Hours: Weekday banking hours. Notary-specific hours may be narrower than general branch hours and are listed separately under the branch's Hours tab.

•Documents: Standard documents. Institutional complexity due to Citibank's global compliance policies adds additional layers of restriction for international documents.

•Exclusions: Many Citibank branches do not offer notary services at all. Estate documents and international documents are subject to additional compliance review and are frequently declined.

Capital One

Capital One provides notary services at its full-service branch locations, not at Capital One Cafe locations. The bank's notary service is a customer benefit and requires an appointment. Capital One's customer service line can be used to identify notary-enabled branches and schedule appointments.

•Account holder requirement: Yes.

•Fee: Free for customers. Some locations may apply state-permitted fees.

•Appointment: Required. Schedule through the branch or by calling 1-877-383-4802.

•Hours: Typical weekday hours Monday through Thursday 9 a.m. to 5 p.m. and Friday until 6 p.m. Some Saturday hours available. Notary service limited to full-service branch locations only.

•Documents: Standard personal and financial documents.

•Exclusions: Not available at Capital One Cafe locations. Notary not available at all branches. Estate planning document exclusions apply.

Fifth Third Bank

Fifth Third Bank offers notary services at many of its branches, with particular emphasis on customers holding Preferred Checking accounts. Availability varies by location, and calling ahead to confirm is strongly recommended before visiting.

•Account holder requirement: Yes. Preferred Checking customers may receive priority access.

•Fee: Free for most customers. Some branches may charge depending on document type.

•Appointment: Recommended.

•Hours: Weekday banking hours. Some Saturday hours available. Hours vary significantly by branch.

•Documents: Standard personal documents.

•Exclusions: Not all branches staff a notary. Estate and complex document exclusions apply consistent with industry norms.

Huntington National Bank

Huntington National Bank provides notary services to its customers by appointment. The bank operates across Ohio, Michigan, Indiana, Kentucky, and several other Midwest and Southeast states. Notary availability is confirmed at the branch level, and an appointment must be made in advance.

•Account holder requirement: Yes.

•Fee: Free for customers.

•Appointment: Required. Listed as appointment-only across sources.

•Hours: Monday through Thursday 9 a.m. to 5 p.m., Friday 9 a.m. to 6 p.m., Saturday 9 a.m. to 2 p.m.

•Documents: Standard personal and financial documents.

•Exclusions: Estate documents subject to standard exclusions. Notary availability must be confirmed at individual branch level.

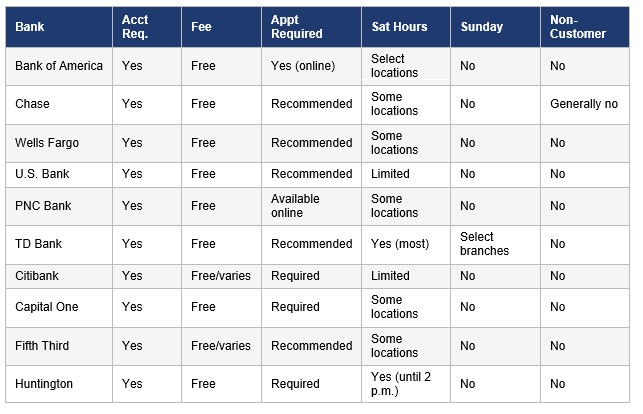

Comparative Summary Table

The table below summarizes the core policy variables across all ten institutions reviewed in this paper.

Req.

Required

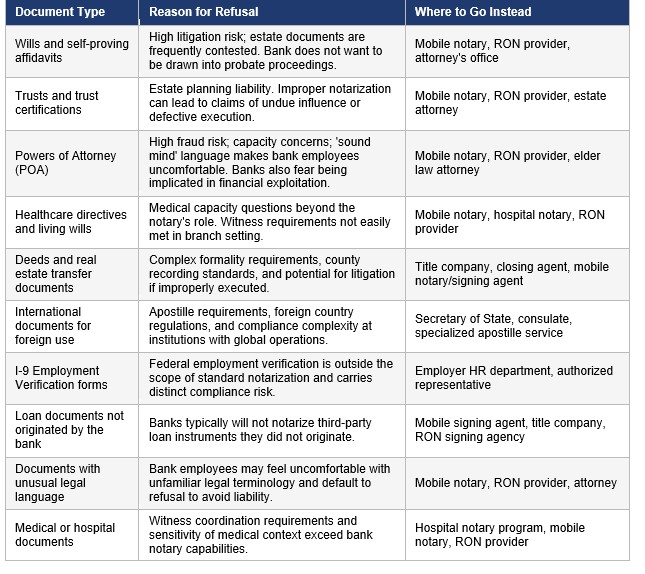

Document Exclusions: What Banks Commonly Refuse to Notarize

One of the most significant and least publicized aspects of bank notarization is the broad category of documents that banks routinely decline to notarize. These exclusions are driven primarily by liability concerns rather than any legal prohibition. A notary employed by a bank is a commissioned state public official, but their employer's internal risk policies frequently override the full scope of what they are legally authorized to do.

Commonly Refused Document Categories

Analysis: The Policy Fragmentation Problem

No Federal Standard Exists

There is no federal law or regulation requiring banks to offer notary services, standardize their policies, or serve any particular class of customer. The decision to offer notarization, and on what terms, is entirely at the discretion of each institution. This means that every policy decision examined in this paper: the account holder requirement, the document exclusions, the appointment rules, and the hours of availability, exists because each bank independently chose those parameters. A different bank chose differently.

The Account Holder Barrier

Every major bank reviewed in this research restricts notary services to existing account holders. This creates an immediate access gap for the following populations: individuals who do not maintain a bank account, individuals who bank with an online-only institution such as Ally, Marcus, or Discover (which have no physical branches), individuals who have a banking relationship with a different institution than the one closest to them, and individuals in rural areas or underserved communities where the nearest branch of their bank may not have a notary on staff.

The account holder requirement is not a customer service feature. It is an access filter. It transforms what many consumers believe to be a public or neutral service into a benefit tied to an existing commercial relationship.

Notary Availability Is Not Guaranteed

Even for eligible account holders who make an appointment at the right branch, there is no guarantee of access. Notary availability at bank branches depends on whether a commissioned notary is on staff that day, whether that employee is available and not assigned to other banking duties, whether the branch has a notary at all (not all do), and whether the branch is open on the day and time the customer needs.

This is not a theoretical concern. Multiple practitioners and consumer sources report showing up to bank appointments only to be told the notary is unavailable, has left for the day, or has called in sick. Unlike an independent notary service or a remote online notarization provider, a bank cannot always staff a reliable substitute.

Document Exclusions Are Extensive and Inconsistent

Perhaps the most impactful finding of this research is the breadth of document exclusions applied across banking institutions. The common perception is that banks notarize documents broadly and conveniently. The reality is that an entire category of the most legally significant documents Americans need notarized, including wills, trusts, powers of attorney, real estate deeds, and healthcare directives, are routinely refused by major banks.

These refusals are not based on any legal prohibition. A commissioned notary is authorized by their state to perform notarization on any eligible document for any eligible signer. The refusals are internal corporate policy decisions designed to insulate the institution from liability. The result is that consumers with urgent estate planning needs, complex real estate transactions, or sensitive healthcare documents are turned away and must find alternative service providers, often under time pressure.

Critically, these exclusions are not applied consistently. One branch may refuse to notarize a power of attorney while a branch of the same bank three miles away will complete it without issue. One notary on staff may feel comfortable with a will while another refuses. This inconsistency makes the banking system an unreliable foundation for any consumer who needs guaranteed, predictable notarization outcomes.

Hours of Operation Limit Accessibility

With the exception of TD Bank, which offers extended evening hours and some Sunday access at select locations, all major banks operate on a Monday through Friday weekday schedule that may include limited Saturday morning hours. There is no major bank that offers consistent evening or weekend notarization access.

For working adults, individuals with caregiving responsibilities, or those facing urgent document needs outside of traditional business hours, bank notarization is simply not a viable option. This is a structural gap that independent mobile notaries and remote online notarization providers are uniquely positioned to fill.

Credit Unions: A Note on Flexibility

Credit unions are frequently cited as more flexible than commercial banks when it comes to notarization. Institutions such as Navy Federal Credit Union, PenFed Federal Credit Union, and State Employees Credit Union offer notary services to their members, typically free of charge. Some credit unions report greater willingness to notarize documents that commercial banks decline, though this is inconsistent.

Navy Federal Credit Union, for example, provides free notarization for Navy Federal-related documents and for up to two additional documents per week at no charge, with a modest fee applied after that threshold. This volume-based approach is unique among the institutions reviewed and reflects a different service philosophy than the commercial banks.

Credit unions are also more likely to maintain consistent staffing of commissioned notaries across their branch network, in part because their cooperative structure prioritizes member services over broad commercial banking functions. However, the member-only access requirement still applies, and document exclusions similar to those at commercial banks are observed in practice.

Online-Only Banks: No Notary Access

A growing segment of American banking customers use online-only institutions that offer no physical branch presence. Banks in this category include Ally Bank, Marcus by Goldman Sachs, Discover Bank, Chime, and SoFi. None of these institutions offer in-person notarization services.

Customers of online-only banks who need notarization must seek out independent, mobile, or remote online notarization services. This segment of the population represents a significant and growing market for RON providers and independent notary professionals.

Conclusion: The Case for Independent and RON Notarization

This research supports a clear conclusion: the American banking system does not provide a standardized, reliable, or universally accessible notarization solution. Each institution makes independent policy decisions that result in a fragmented landscape where:

•All major banks restrict service to their own account holders, excluding a substantial portion of the public.

•No bank guarantees notary availability at every branch or at all times.

•Every bank applies document exclusions that eliminate the most legally significant documents from their notarization scope.

•Hours of operation restrict access to weekday business hours for the vast majority of banking consumers.

•Enforcement of policies varies by branch, by region, and by individual notary.

These gaps are not coincidental. They are the product of deliberate policy choices made by institutions whose primary business is banking, not notarization. The result is a service that is free but unreliable, available but restricted, and offered but inconsistently honored.

For consumers who need dependable, document-inclusive, and time-flexible notarization services, the banking system is not the answer. Independent mobile notaries, signing agents, and remote online notarization providers fill each of the gaps identified in this research: they serve any client regardless of banking relationship, they typically notarize the full scope of eligible documents, they are available evenings and weekends, and they provide consistent and specialized service that banks cannot deliver.

The argument that banks provide a sufficient and complete notarization solution for the American public is not supported by the evidence. One size does not fit all, and for millions of Americans, the bank is not the right fit at all.

Sources and References

The following sources informed the research and findings presented in this paper:

•Bank of America Official Notary Services Page: bankofamerica.com/signature-services/notary

•Bank of America Appointment FAQ: secure.bankofamerica.com/secure-mycommunications/public/appointments/faq

•Chase Bank Notary Services Overview: coincodex.com and bluenotaryonline.com (comparative review)

•Wells Fargo Notary Services Policy: wells fargo.com (branch locator and services tab)

•LegalClarity: Do Banks Have Notary Services? legalclarity.org (April 2026)

•LegalClarity: How Much Does It Cost to Notarize a Document at a Bank? legalclarity.org (April 2026)

•BlueNotary: Do Banks Notarize Documents? bluenotaryonline.com

•BlueNotary: Banks That Notarize for Free: Complete List. bluenotaryonline.com

•First Quarter Finance: 22 Banks and Credit Unions That Have Notaries. firstquarterfinance.com

•Frugal Answers: List of 20 Banks with Notary Service. frugalanswers.com

•KYZ Law: Why Banks Refuse to Notarize Estate Documents. kyzlaw.com (June 2025)

•eNotary on Call: Why Banks Won't Notarize Your Will. blog.enotaryoncall.com (February 2026)

•Trust and Will: What to Do If a Bank Won't Notarize Your Estate Planning Documents. trustandwill.com

•Treasure Coast Notary Service: 7 Reasons Why Banks Won't Notarize Certain Documents in Florida. treasurecoastnotaryservice.com (December 2025)

•ProActive Mobile Notary: Why Banks Are Reluctant to Notarize Power of Attorney or Wills. notaryhannah.com

•NotaryCam: Do Banks Have Notaries? notarycam.com (January 2026)

•Notarize.com: Finding a Fifth Third Bank Notary Near Me. notarize.com

•CheckDeposit.io: Does Capital One Offer Notary Services? checkdeposit.io

•Looking Glass Runners: Why Banks Don't Always Offer Notary Services Anymore. lookingglassrunners.com (October 2025)

•Las Vegas Mobile Notary: Do Banks Notarize Documents in Las Vegas? lakemeadmobilenotary.com (October 2025)

© 2026 Notary SWFL - All Rights Reserved

We are not attorneys and do not provide legal advice or representation.